| | April 18, 2024 |

|

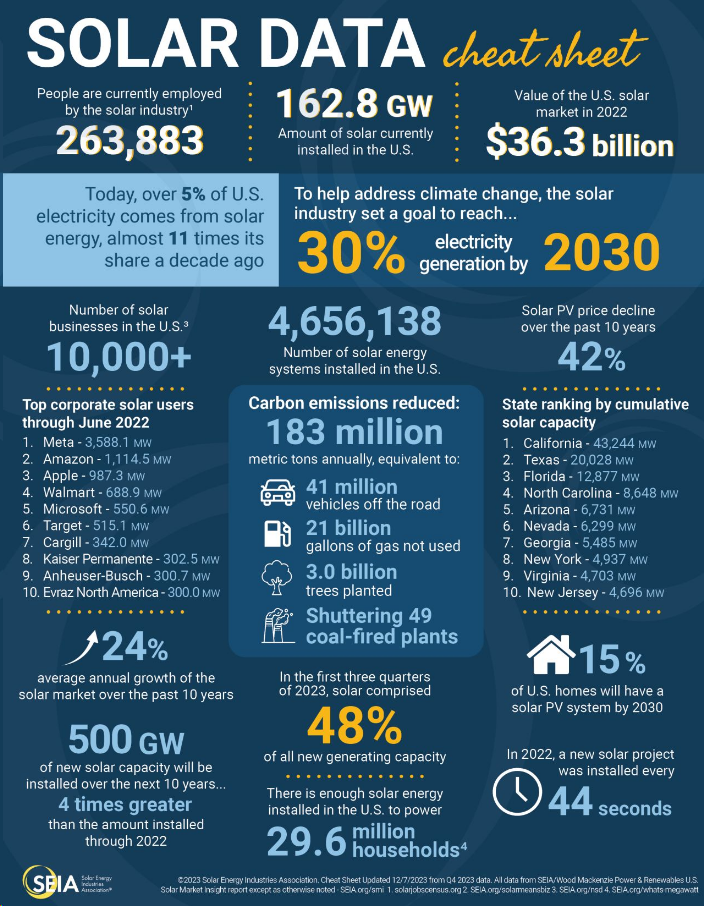

In Q3 2023, the U.S. solar industry witnessed substantial growth, adding 6.5 gigawatts (GW) of new electric generating capacity, marking a noteworthy 35% year-over-year increase. The U.S. Solar Market Insight Q4 2023 report, jointly released by the Solar Energy Industries Association (SEIA) and Wood Mackenzie, projects that the United States is poised to achieve a record-breaking addition of 33 gigawatts (GW) of solar capacity in 2023, fueled by the positive impact of federal clean energy policies. Despite encountering economic challenges affecting the solar and storage sector, solar is projected to become the largest source of generating capacity on the U.S. grid by 2050.

Noteworthy achievements include the residential solar segment, which set a record by installing 210,000 systems in Q3. However, anticipated shifts in net energy metering policy in California and increased interest rates across the U.S. are anticipated to temporarily slow growth in the coming year before a resurgence in 2025.

Elevated financing costs, transformer shortages, and interconnection bottlenecks have impacted the utility-scale segment, experiencing its lowest level of new contracts signed in a quarter since 2018. Nevertheless, improvements in the module supply chain resulted in a remarkable deployment of 12 GW of utility-scale capacity in the first three quarters of 2023.

Solar now contributes to 48% of all new electric generating capacity added in the first three quarters of 2023, elevating the total installed solar capacity in the United States to 161 GW across 4.7 million installations. The report foresees solar capacity in the United States reaching 377 GW by 2028, sufficient to power over 65 million homes.

Michelle Davis, Head of Solar Research at Wood Mackenzie and lead author of the report, emphasized the robust growth trajectory of the U.S. solar industry, projecting a 55% growth in 2023 and a subsequent 10% growth in 2024. Davis emphasized the industry's need for ongoing innovation to navigate challenges such as interconnection constraints. Key tools for future success include interconnection reform, regulatory modernization, and an increased focus on storage attachment rates. Leading the nation in Q3 solar installations were California and Texas, with Indiana securing the third position by adding 663 megawatts (MW) of new capacity, primarily from large utility-scale projects coming online. A total of 14 states and Puerto Rico each installed over 100 MW of new solar capacity in Q3.

(Reference: SEIA)  |

Try our iDesign BOM Calculator.....